Some thoughts on Vibe Coding, SaaS vs AI (10 Moats) and Guidewire Software

Executive Summary:

This post does not contain any actionable investment advice but rather some personal ramblings on Vibe coding and the attempt to analyze a specific Software company (Guidewire) according to a Template of 10 Moats for Software companies and their vulnerability to the AI threat.

Introduction:

My track record as a Software investor is to put it mildly, very poor. My best Software Investment so far is Chapters Group which I bought as a net-net before it even became a VMS Serial Acquirer. My blog and portfolio archive also tell me that I sold Microsoft in 2011 at ~25$ per share with a 4% gain because I thought that the Office products had no future. So please take everything I say about Software with a grain of salt or even better, just ignore it.

I do have a background in Software development. Although I would not call it Software development but “Code butchering”. It started as a teenager on a C64 with Basic and Assembler and ended in the late 1990s with Cobol/PLSQL working for a large US Consulting Company (yes, I was young and needed the money). Knowing the speed of financial institutions, I would not be surprised if some of my Spaghetti code would still be running somewhere….

Why am I saying this ? Because of course, Software stocks have been doing quite poorly over the past weeks/months. In addition, I also had the opportunity to play around with Claude Code first hand.

Already last year, I used ChatGPT to create little computer games, which was quite cumbersome and only worked partially. This time around, with Claude Code, I suddenly became the hero of my little son as I created the computer game that he “invented” and wrote down on a piece of paper. It is a simple but very playable horizontal scrolling game with a Monster Truck where you can gain points with crazy jumps and crashing cars.

Here are two maybe not so impressive screenshot but the game is really fun:

Other than last year, this one worked at the first attempt and improving the game (.i.e. creating different worlds, adding explosions, changing gravity etc) just requires a few prompts. Of course this will never be competition for the Nintendo Switch that Santa Clause failed to deliver this Christmas, but it is pretty obvious how good those tools already have become. The initial version of ChatGPT has only been released like 3 years ago.

I think this is one of the fascinating aspects of the whole “AI Saga”: You can theorize a lot about AI but at the same time, everyone can pay 20 bucks a month and test the best tools himself or herself.

So is SaaS & Software now dead or what ?

The short answer in my opinion is: “nobody knows anything”. I have read a lot of well written pieces where investors either argued that Software will never be endangered by AI and now is the time to go all in. Or pieces that claim that in 12-18 months it is all over.

Often those pieces reflect a vested interest of a VMS Serial Acquirer investor ($CSU bulls fo instance) or from an AI dude who is obviously bullish.

Only in very rare cases does one get a more nuanced view like this post to which I already linked in the latest “some links” post. More on this later.

Here are some things I think:

Even for the best AI experts, it is extremely difficult to truly predict how the capabilities of the models will evolve over the next 1,3,5 or even 10 years. Maybe they hit a ceiling, maybe they develop exponentially. In the past, those developments initially took longer than expected but then accelerated at some point in time

Software bulls often argue that no customer will “vibe code” an application. I think that is correct but that doesn’t protect Software companies from competitors, especially from the AI labs themselves

The AI labs themselves are basically forced to get into the “application layer”, otherwise they might end up as exchangeable API call providers where it will be super hard to earn a return on the multi trillion investments

History often created losers and winners from such structural shifts. I think it makes a lot of sense to look at all this with a differentiated point of view.

Overall, uncertainty for Software stocks clearly has increased which needs to be reflected in valuations. And I guess that is what is currently happening

Just because a stock dropped -50% or more doesn’t mean that it is cheap looking 3-5 years into the future.

Let’s have a quick look at Guidewire Software

Guidewire is a US based Software company that was founded in 2001 and went public in 2012, so before most of the current “SaaS Superstars”. I have been looking at the company from time to time, as I have encountered it a couple of times in my professional career and roughly understand what they are doing.

Guidewire is a very specialized Software company as it provides basically the “operating & production” system for a P&C Insurance company. Many Insurance companies used to code their own systems which got super complex after mayn years and really hard to maintain. Therefore, over time many Insurance companies were looking for standardized products as their inhouse systems became harder and harder to keep up.

Sales cycles to replace Insurance Core systems are very long, as such a “heart transplant” is always messy, very expensive and not seldom has failed in the past. I read some statistics that only 1 out of 4 “core system” exchanges were successful in the insurance industry.

Despite or because of this, Guidewire has achieved market share of over 50% in the US and also its international presence is growing.

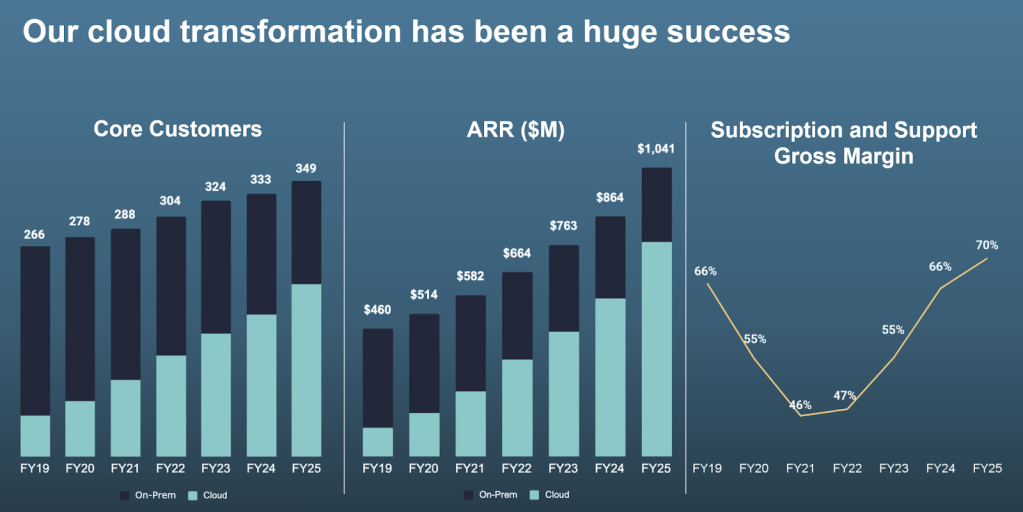

Being a rather “old School” Software company and knowing how conservative Insurance companies are, it is also not a surprise that still a lot of their revenue is “on premise” and that the transformation to “real SaaS” is still ongoing:

Is Guidewire now doomed ?

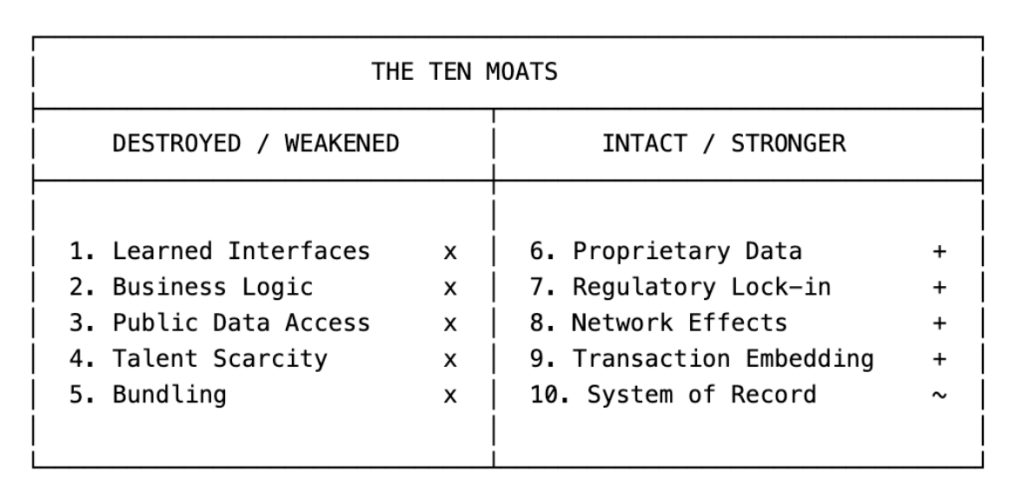

This is the “Moat table” from the post that I linked to in the beginning:

I think Guidewire clearly relies partially on the moats on the lefthand side with the exception of Public Data Access which to my knowledge is not so relevant.

On the other hand, all moats from the right side apply to Guidewire, especially the proprietary data (claims etc.) and regulatory lock -in as Insurance is maybe one of the business sectors with the highest degrees of regulation.

A typical Guidewire system is also deeply integrated into an insurance transaction and of course the ultimate system of record. The only moat that I don’t see so strong is the network effect.

So overall I would say that Guidewire exhibits some of the moats which are quite hard to penetrate from AI for the time being.

What has been issued by the big AI labs so far ?

One news item from a few days ago that made some waves was a “ChatGPT app” called Insurify which seems to be a front end of an already existing retail Insurance comparison service in the US. From some discussions on Reddit it seems that this is much more a front end than an “end to end” platform. For some reasons that I never fully understood, Americans don’t really like to compare insurance quotes anyway. At leat not to the extend that for instance the Brits do. But in any case, this one clearly doesn’t look like a disruptor.

A more interesting approach comes from Anthropic who has announced cooperations with Travelers and Allianz in recent weeks.

I think this is clearly the attempt from Anthropic to enter the application layer in insurance but it needs to be seen if and how this could become some kind of competition to Guidewire.

Travelers seems to be a Guidwire client. It will be interesting to see if and to what extent this impacts Guidewire’s ability to sell additional modulus and functionalities to existing clients for instance.

Is Guidewire a buy at current price levels ?

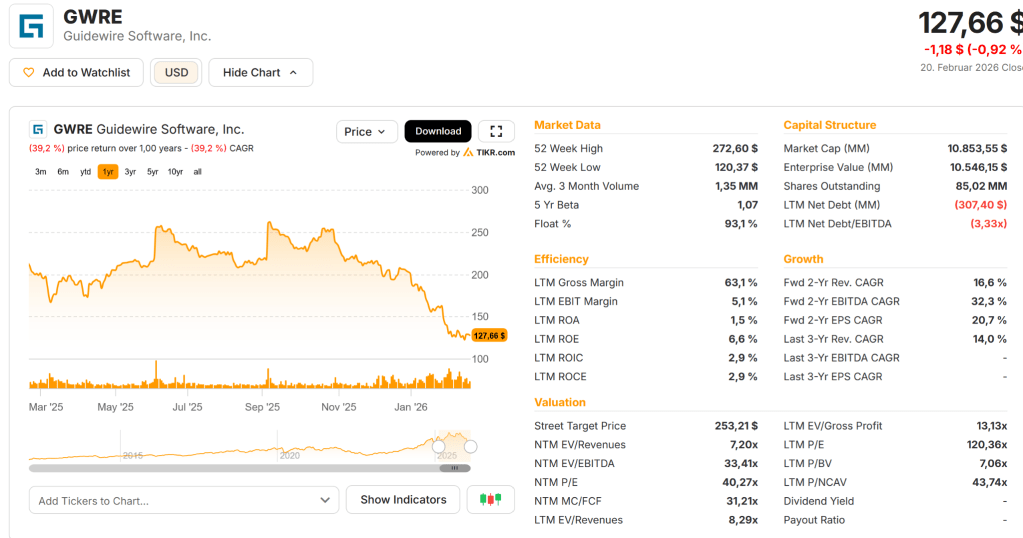

Looking at Guidewire’s stock chart we can see that the stock lost around -50% from its peak just a few months ago:

So the question clearly is: Is Guidewire no a good investment looking forward a few years ?

Looking at the TIKR overview we can see that Guidewire trades at 120x LTM P/E and around 40x NTM P/E

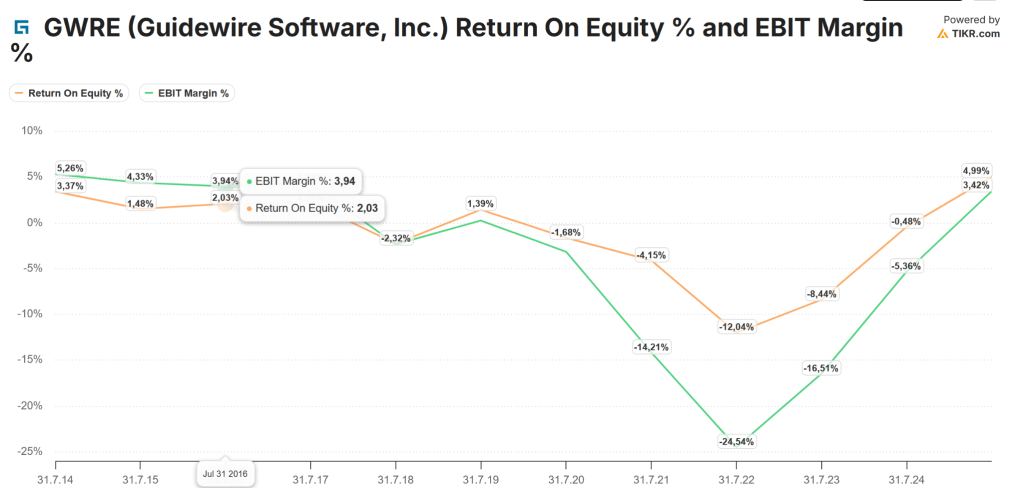

This is clearly not cheap. Returns on investment and margins are historically quite low:

The culprit here, as with many other Software stocks, of course, is share based compensation (SBC).

Guidewire currently earns Gross margins of around 60% but pays out ~15% of sales as SBC. Including SBC, they ran at an operating loss.

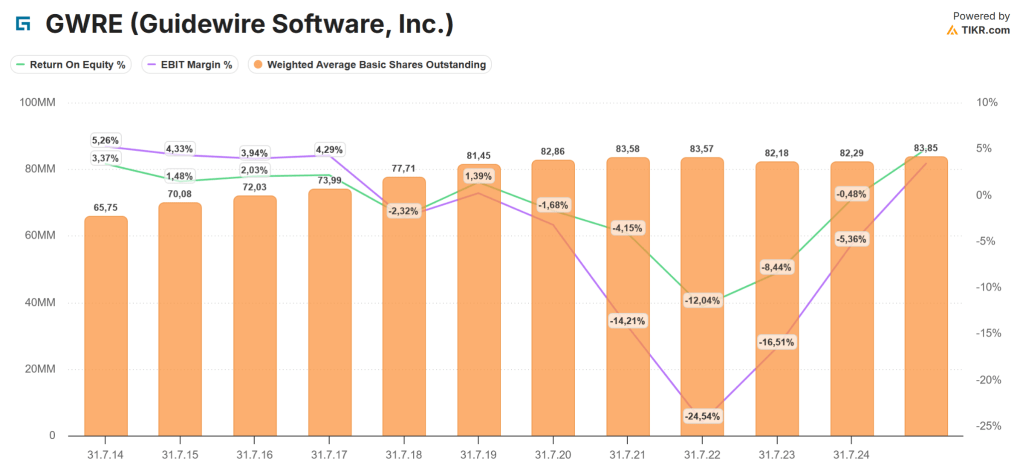

This chart also has the average outstanding shares included. It clearly shows that despite share repurchases, the number of shares has been going up, although at a slower pace in the last few years.

With regard to operating cash generated, nothing went to shareholders but rather everything and more went to the employees, which seems to be the norm for many US based SOftware companies.

Top line growth has been ~+12% for the last 10 years and ~+10% for the last 5 years. Pretty Ok, but not outrageously high.

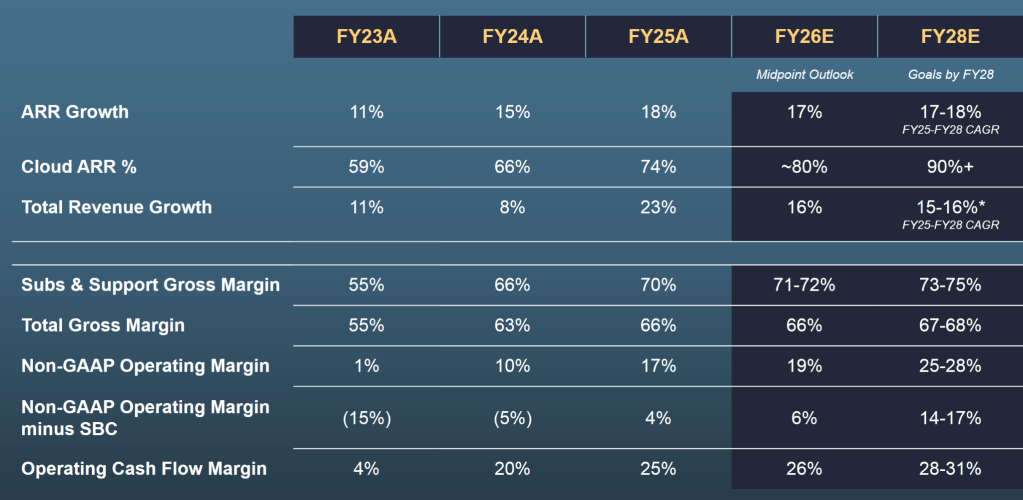

In a recent investor presentation, Guidewire gave the following guidance:

If we take the upper end of the prediction (16% total revenue growth, 17% operating margin) we get to a target “Non-GAAP” Operating profit after SBC of ~320 mn USD.

Based on today’s EV of 10,5 bn USD and assuming no further dilution, Guidewire trades at 33x 2028 EV/EBIT.

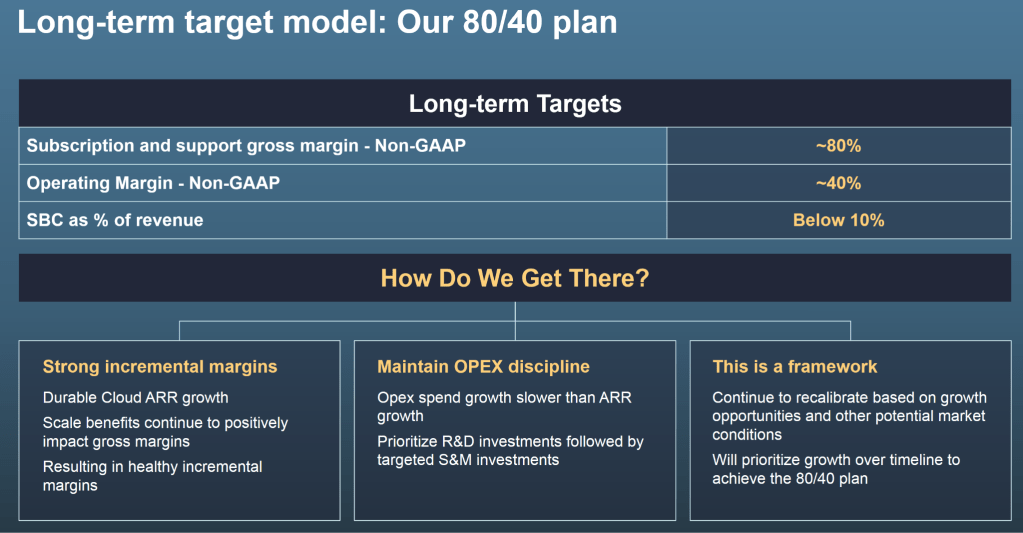

They also give a “long term guidance” which looks like this:

But to be honest, I would not want to underwrite such a generic “guidance” without a measurable target date.

Now I am clearly not the right investor to pay 33x EV/EBIT for any company. In Guidewire’s case, the nearer future looks pretty safe, but a valuation like this requires that very little negative impact will happen for quite a long time.

One scenario could be that Guidewire benefits for instance as the cumbersome implementation process might become easier with AI tools but that would be clearly speculation for now.

What I find interesting is that many Software investors still argue with the “Rule of 40”, EV/ARR or Operating Cash Flow yield multiples which might be historically at relatively low levels. But at the end of the day, investors need “free Cashflow after SBC” or “GAAP earnings”. And many software stocks still look very expensive with regard to these traditional metrics.

Just as a side note: German IT Consultant GFT Technology seems to be a strategic Guidewire implementation partner. The company isn’t doing that well either lately, but Insurance is only around 15% of the business:

So summarizing it at this point my take-away would be as follows:

Yes, Guidewire, for now, looks relatively safe from direct AI competition for some time due to the complexity and regulatory requirements of such systems

However, and that’s a big however, the stock is anything but cheap on traditional metrics, even assuming the high end of the companies’ projections.Nevertheless, I do like the Framework provided with the 10 moats to analyze other Software companies in the future

Interestingly, many market participants still only look at “funny metrics” instead of traditional valuation metrics.

Bonus Soundtrack:

Of course there is also a Bonus song for this post. This time the Trammps with the (justified) question: Where do we go from here ?

Thanks for your point of view.

Just one question regarding „proprietary data“. I am not sure whether your given example with claims data applies. The data is certainly in the Guidewire software but I would doubt that Guidewire is allowed to use it and eg sell it to other insurance companies. However, I don’t know their contracts so maybe they are.

Looking forward to your next article.